Oops! Something went wrong while submitting the form.

Our Founding Partner, Ben Yoskovitz asked a group of corporate innovators why they believe internal innovation is so hard. After hearing the many reasons why, he shared his insights for a less risky alternative, the corporate spin-out.

Everyone is familiar with the phrase “innovate or die,” especially in corporations where continuous growth is expected but elusive.

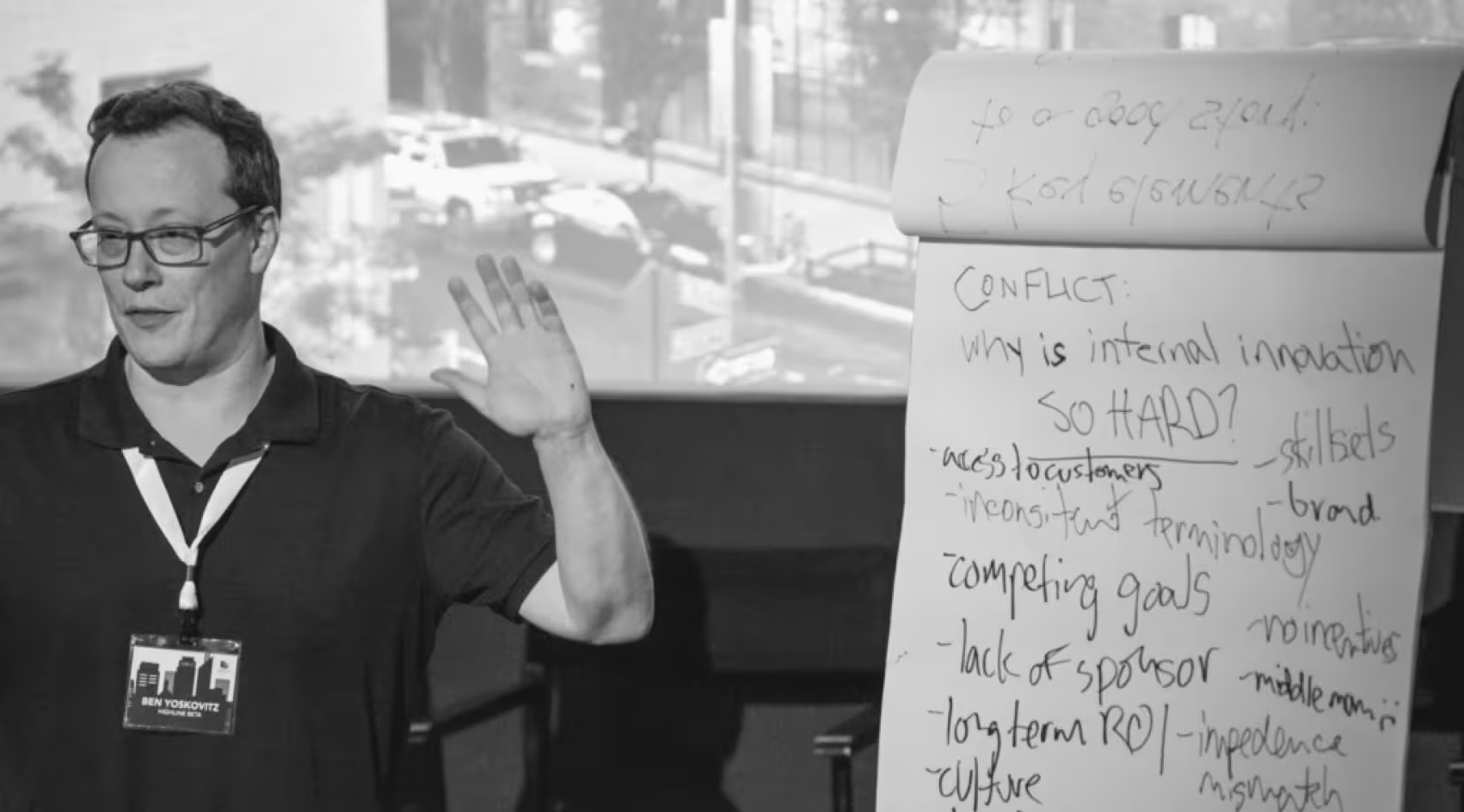

At a recent conference, I asked a group of corporate innovators, “Why is internal innovation so hard?” I got a lot of responses. As people shouted answers out, I scribbled as fast as I could while many others were nodding their heads in agreement.

The roadblocks to innovating — in particular when you’re focused on emerging growth outside of your core line of business — are significant. And realistically, all the innovation frameworks, operating models or systems in the world, can’t completely solve these problems. Interestingly, every big company struggles with the same challenges, but you can’t implement a top-down cookie cutter solution and expect it to work.

During the talk, I proposed an alternative to internal innovation that can solve many of these challenges: the spin-out. A spin-out is a new venture that starts internally, but then becomes a separate, independent company on the outside.

This is not to suggest that companies should stop innovating internally. I don’t believe companies can completely outsource innovation, and they have an obligation to keep working on internal innovation, particularly the more transformative innovation that’s further from the core. But recognizing that it’s incredibly difficult to innovate on the inside, spin-outs provide another useful tool in the toolbox.

There’s no one way of spinning out a company, and no formula for success, but there are a number of key considerations:

It solves a few of the key challenges highlighted by the group of corporate innovators:

Competing goals: This is no longer an issue because the startup is on the outside focused on its own goals. And the best spin-outs are those that have a meaningful corporate relationship creating an unfair advantage.

Culture, Capacity, Skill Sets & Incentives: When a startup is spun-out, a new CEO is brought on board and then a new team is hired. The new startup can build its own culture and hire for the people & skill sets it needs to succeed. Additionally, the startup offers potential upside in the form of equity. Internal innovation opportunities rarely have a model for incentivizing the effort or perceived risk of building something new in-house.

Money & Failure: Spending money on incubating new ventures is a challenge for big companies, but most are able to do it. However, their comfort level with failure is almost always very, very low. And new ventures fail, which is why we always recommend building a portfolio. When a spin-out fails it still hurts, but the burden is less on the corporate partner as the risk has been shared with other investors. Venture studios should co-invest with corporate partners. Other angel investors or venture capital investors may also invest if they see the potential. At the earliest stages this may not seem terribly important, but when that startup is looking to scale and needs millions and millions of dollars in funding, a big company may shy away from spending that money. It may be hard to make the business case if you’re looking to spend that on a seemingly high-risk opportunity, especially if it remains on the inside. Big companies will look at that spend as a cost, not an investment. Venture capital investors are there to make investments.

Big companies often debate whether they should build, buy/acquire or partner. While all viable options, the spin-out should be an equal fourth option. Interest in how spin-outs work is increasing because of the challenges inherent with the other options, especially internal innovation and building new ventures.

Spinning out startups isn’t the answer to every challenge faced by corporate innovators, but it is a legitimate tool that big companies can use in creating a balanced portfolio of innovation opportunities and new ventures.

Ultimately, internal innovation is hard, and that’s not changing any time soon. And while it’s a necessary effort and can help companies grow and win, spin-outs solve a lot of the problems faced by internal innovation and are an interesting additional way of building emerging growth businesses.